A First-time Home Buyer’s Guide to Mortgages

Thinking of buying your first home by getting a mortgage, but don’t know where to start? Here is a break-down of the absolute must-knows from mortgage rates to first-time home buyers benefits, and everything in-between. Pull out your pen and paper because you’re about to do some hands-on math exercises, or if you’re uncomfortable hearing the word “math”, there is a handy calculator and even someone to help you…just keep reading along!

What are mortgages?

Picture your dream home with a freshly cut yard and a world-class kitchen that top chefs would envy. It’s a perfect house for you and your future family. The house is quoted to you at a price of $450,000. On top of your bills and debt obligations, you must be wondering, “Woah, there is no way I can save up that much money!”.

That’s precisely why there are mortgages.

Mortgages are used to make large real estate purchases without having to fork-out the entire value of the house. Mortgages are loans where you borrow your money from your credit union, and then repay the loan (with any applicable interest) until you’ve paid off the principal.

In a typical mortgage structure, the borrower puts a downpayment of 20% of the entire value of the house and borrows the remaining 80% on a 15- or 30-year repayment term.[1]

Types of Mortgages

Shopping around for the right kind of mortgage could really save you thousands in the grand scheme. Given that this is going to be the single biggest purchase of your life, it’s worthwhile to learn what’s out there to see what suits your situation the best.

1. Fixed Rates or Adjustable Rates

Fixed-Rate Mortgages, as the name implies, are rates that stay the same for the entire repayment term. Your monthly mortgage payments per month will always be the same throughout the repayment period.

On the other hand, an Adjustable Rate Mortgage (ARM) are loans where the rates are fixed and set below the market rate for the first few years and adjusts to a higher rate as time progresses. Typically in 3, 5 or 7 year increments. For example, your lender will usually advertise a “5/1 ARM 30-year mortgage”. The “5” refers to the number of years at a fixed rate, and the “1” refers to how often the rate will adjust after that.

Some of the advantages of adjustable rates are:

- Monthly mortgage payments are less in the initial years and you could get more house given that the rates start below the current market rate.

- If you’re lucky, the market rate adjustment could be even lower than your initial quoted rate, giving you a nice discount on your monthly mortgage payments, saving you thousands in the long-run.[2]

2. Conventional Loans or Government-Insured

Conventional loans are loans that are not government insured. When you default or fail to make payments on the loan, the lender loses money. Therefore conventional loans require a stringent qualification process consisting of three factors: stable income, good credit and size of down payment.

Government-insured loans are loans that are, as the name implies, insured by the government. Since these loans are insured and backed by the specific governmental programs themselves, it is easier to qualify for a loan.

Some popular government-insured loans include FHA, USDA and VA loans. Let’s take a look into each one of them:

- Federal Housing Administration (FHA) loans

An FHA loan is a mortgage loan that is insured by the FHA. It is popular because this type of loan allows one to borrow with only a 3.5% down payment, as opposed to the usual 20%. It also allows people with a credit score of 580+ to qualify. For credit scores as low as 500, a 10% down payment is the minimum needed to qualify.[3]

Because an FHA loan does not have the strict standards of a conventional loan, it requires two kinds of mortgage insurance premiums: one is paid in full upfront or it can be financed into the mortgage, and the second is an annual premium which is paid monthly.

Upfront premium: 1.75 percent of the loan amount is paid when the borrower gets the loan. This premium can be rolled into the financed loan amount.

Annual premium: The rate varies between 0.45 percent to 1.05 percent, depending on the loan term, the loan amount and the initial loan-to-value ratio. This premium amount is divided by 12 and paid monthly.[4]

Learn more about FHA requirements and other additional information.

- U.S. Department of Veteran Affairs (VA) loans

The U.S. Department of Veterans Affairs (VA) helps active-duty military members, veterans and surviving spouses buy homes. VA loans are very popular, if the borrower is eligible, because it is a zero-down-payment mortgage with competitive interest rates and doesn’t require a minimum credit score.

Learn more about VA loan requirements and other additional information.

- U.S. Department of Agriculture (USDA) loans

The United States Department of Agriculture created this program to promote home ownership in rural communities across the U.S. Don’t let the word “rural” fool you because the areas eligible for this program cover an estimated 97% of the U.S.

USDA loans are similar to VA loans in that it is a 100% financed, with zero-down-payment, mortgage. Because of this, it is one of the most attractive programs out there in the market today.

Learn more about USDA loans and your eligibility.

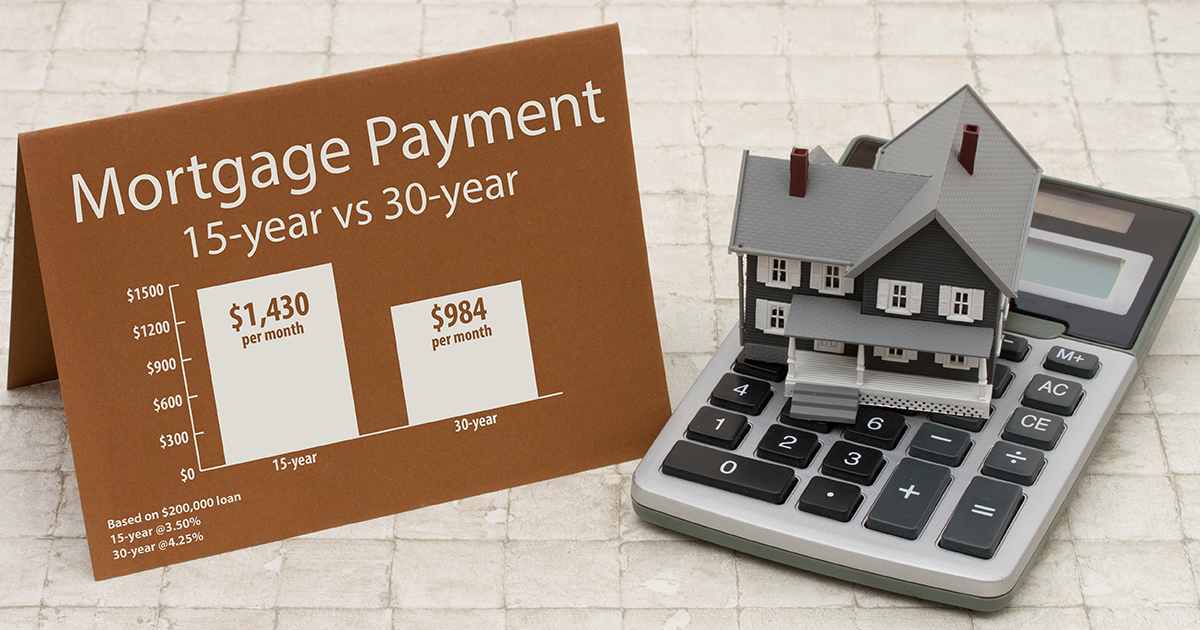

3. 15-year or 30-year mortgages

15- and 30-year terms both have their advantages depending on your financial plans and unique situation. A 15-year term will sport lower interest rates, but will incur higher monthly payments. Since you’ll be paying off the house in half the time vs. the 30-years, you’d be able to save yourself a considerable sum.[5]

15- and 30-year terms both have their advantages depending on your financial plans and unique situation. A 15-year term will sport lower interest rates, but will incur higher monthly payments. Since you’ll be paying off the house in half the time vs. the 30-years, you’d be able to save yourself a considerable sum.[5]

To illustrate this idea better:

Value of house: $450,000 • 20% downpayment: $90,000

| 15-year term* | 30-year term* | |

|---|---|---|

| Mortgage Rates | 4.0% | 4.5% |

| Monthly Payment | $2,663 | $1,824 |

| Total House Cost | $479,319 | $606,502 |

*The above is for illustrative purposes only. Actual payment information may vary. Rates are show for illustrative purposes only and may vary due to individual credit worthiness and or loan term. Payments may vary from final loan payment provided by Empeople loan representatives. You can use our mortgage comparison calculator to compare two different mortgage loans of different repayment terms.

Which mortgage is a good fit for me?

Since every individual and family’s needs are different, having a professional mortgage advisor with deep knowledge and understanding to create more personalized consultation is highly recommended. At Empeople, we have a mortgage team in place to assist and educate our members from start-to-finish so you won’t have to worry about anything.

This is most likely the biggest purchase of your life, therefore it’s always a good idea to have a couple opinions, especially a knowledgeable and experienced one to make sure you make the best decision possible for you and your family’s future.

How do you know if you will be approved for your first mortgage?

It seems daunting at first, but it’s actually an easy and straightforward process once you have a few key figures in your hands. We’ll take you through an example to illustrate how quickly you, too, can master this process.

Let’s meet Jim, a 28-year-old manufacturing company manager who, along with his wife and two young children, is eyeing a $450,000 dream home. First things first, Jim must go through a quick 6-step process in order to best qualify him for his first mortgage loan.

Step 1: Calculate your monthly income.

Jim starts by documenting his monthly income. His lender wants to see at least 2-weeks worth of his most recent pay stubs. Jim makes a comfortable $60,000 a year pre-tax, and his wife is self-employed, owning a business selling knitted goods where she makes roughly $30,000 a year pre-tax.

Their total income amounts to $90,000 a year, which translates to $7,500 per month.

To collect this information, Jim reaches out to his Human Resource Department for his latest pay stubs. As for Jim’s wife, since she is self-employed, she will need to locate and prepare her previous year’s tax filings.

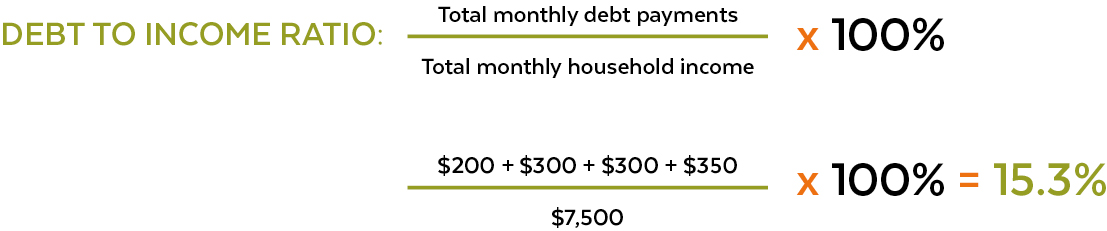

Step 2: Calculate the total sum of your monthly debt payments.

Jim and his wife sit down to discuss their monthly debt obligations. Jim has an auto loan in which he obligated to make a $200 payment per month. In addition, he also has to pay $300 per month on his student loans.

Jim’s wife also took out a small-business loan to the tune of $25,000 whereby she is obligated to a $300 per month loan payment.

On top of that, Jim and his wife both have combined credit card debt currently amounting to $7,000. Most lenders will assume that you’re making monthly repayments of 5% on credit card debt, making it roughly $350 per month.[6]

So the total monthly debt payment for Jim’s family is $1,150.

Step 3: Calculating your debt-to-income ratio.

Now that Jim has his two very important figures, his total pre-tax income and current debt. It’s time to put two-and-two together. Currently, the maximum debt-to-income ratio most lenders will allow is 43%. An ideal range to have is at or below 36%. Of course, the lower your debt-to-income ratio, the better.[7]

With some number crunching, Jim got a 15% debt-to-income ratio. Does it mean he gets a thumbs-up and approval for his loan? Not quite yet.

With some number crunching, Jim got a 15% debt-to-income ratio. Does it mean he gets a thumbs-up and approval for his loan? Not quite yet.

Step 4: Check on your credit scores along with any credit issues in the past.

The three credit bureaus, Experian, TransUnion and Equifax, each give you one free credit report every 12 months.[8] Comb through each report to check your FICO scores and make sure there are no fraudulent activities that you weren’t aware of.

If you have any credit issues that are reported by mistake from the credit bureaus, you can submit a dispute, and work with the credit bureaus to rectify these discrepancies.

Step 5: Calculate how much cash you can put down.

Since Jim and his wife has their sights set on a $450,000 house, and decided to put a 20% down payment on it, they would have to save up a total of $90,000. Still a hefty amount, but a lot more manageable.

Since saving for a down payment could take many years, you’d want to be able to place the money somewhere safe that could still generate a good return, while keeping the funds relatively liquid, such as a money market account, or a CD with high return rates and completely reliable that has a fixed maturity date for those who tend to have a lower self-control for spending.

Step 6: Can you afford the monthly mortgage payment?

A big kitchen ✔️. A backyard space ✔️. Great neighborhood and good schools ✔️! We all know how exciting this can be. You have been diligently saving to finally put in that 20% down payment and are ready to take the final step towards homeownership.

You’re eager and excited but you’ll have one final important calculation to make in order to call that home yours. With your current income, can you pay the monthly mortgage payment for this house, in other words, can you afford a home at this price?

After using a mortgage payment calculator, Jim found out that his monthly mortgage payment is $2,000 per month. The rule of thumb is no more than 28% of your gross monthly income goes to your monthly mortgage payments.[9] Can Jim afford that $2,000 monthly mortgage payment?

If you recall, Jim and his wife both have a monthly income of $7,500.

To afford the $2,000 monthly mortgage payment, Jim must do a quick calculation by taking their Total Monthly Household Income and multiplying it by 0.28.

$7,500 x 28% = $2,100.

Given that Jim’s monthly mortgage payment is expected to be $2,000, he jumps for joy with $2,100.

Hidden fees and expenses you must know when buying a house

Now that you’re an expert at getting mortgages approved and calculating your home budget, the biggest and most common mistake most people forget is ignoring the true cost of home ownership. From closing costs to home inspections, be sure that you’ve covered all your bases before making the plunge.

A big purchase like a house comes with many unforeseen expenditures that you may have missed. Therefore it’s critical to factor in an additional 5-8% of the total home price to cover those extra expenditures.[10] Here’s a comprehensive checklist to make sure you’re not in for any financial surprises:

| Before | After | Other |

|---|---|---|

|

|

|

We hope you were able to get most of your questions answered with this guide. The important thing about making a big financial decision, such as buying a home, is that you have to start planning and learning all the details early. By reading this blog, you’re already halfway there. At Empeople, we offer great rates on mortgage loans. Additionally, as a member of Empeople, you can go to the Online Mortgage Loan Center that is located via Digital Banking to find more information about purchasing or refinancing a home along with the latest mortgage rates. Plus, you can sign up for an email notification system that will inform you of rate changes. Happy home hunting!

Sources:

[1] Investopedia – Understanding the Mortgage Payment Structure

[2] Home Guides – The Advantages & Disadvantages of Adjustable Rates Vs. Fixed Rate Mortgages

[3] Zillow – What is an FHA Loan? – The Complete Consumer Guide

[4] BankRate – What is an FHA Loan?

[5] Investopedia – The 30-year and 15-year mortgages: A comparison

[6] The Mortgage Reports – This Credit Card Rule Makes Mortgage Qualification Easier

[7] SmartAsset – What’s the Ideal Debt-to-Income Ratio for Mortgages?

[8] Consumer Finance – How do I get a copy of my credit reports?

[9] Interest.com – How Much House Can You Afford?

[10] The Balance – 5 Expenses That Shock First-Time Homebuyers