FICO® score vs. credit score. What is a FICO score?

We all know a good credit score is essential when it comes to applying for a credit card, an auto loan, or a mortgage. When a company or a lender checks your credit report, they may be getting it from one or more of the three major credit bureaus – Equifax, Experian, or TransUnion. In addition to your credit report, they will also use a credit score, such as the FICO® score, and self-reported supplemental information, such as your income, in their evaluation of credit risk before lending money to you. Each lender has its own process and policy for deciding upon creditworthiness.

So, what exactly is a FICO score? How does it work? And what is the difference between a credit score and a FICO score? We’re here to clarify this financial term, and answer some of the most frequently asked questions about it.

Credit scores vs. FICO scores

There are many different credit scores, but the main difference is that not all credit scores are FICO scores. A FICO score is simply a brand that was introduced by a company called Fair Isaac Corporation.

Whether it’s a FICO score or not, all credit scores measure your credit risk. The lower your credit score number, the more creditors or lenders will view you as a high-risk investment. Credit scores are based on each individual credit report’s algorithm, so each report can generate different scores. Hence, you could have hundreds of credit scores without even knowing it. Unless it’s clearly marked as a FICO score, you could be viewing a different credit score report. However, it’s more likely you will be most familiar with your FICO score – and with good reason.

What are FICO scores?

FICO scores are the credit scores most widely used by lenders. In fact, they are used in over 90 percent of U.S. credit lending decisions. By knowing your FICO score, you can understand how financial institutions and lenders evaluate your credit risk when you apply for a loan or a credit card.

Each FICO score is a three-digit number calculated from the data on your credit reports at the three major consumer reporting agencies Experian, TransUnion, and Equifax.

How are FICO scores calculated?

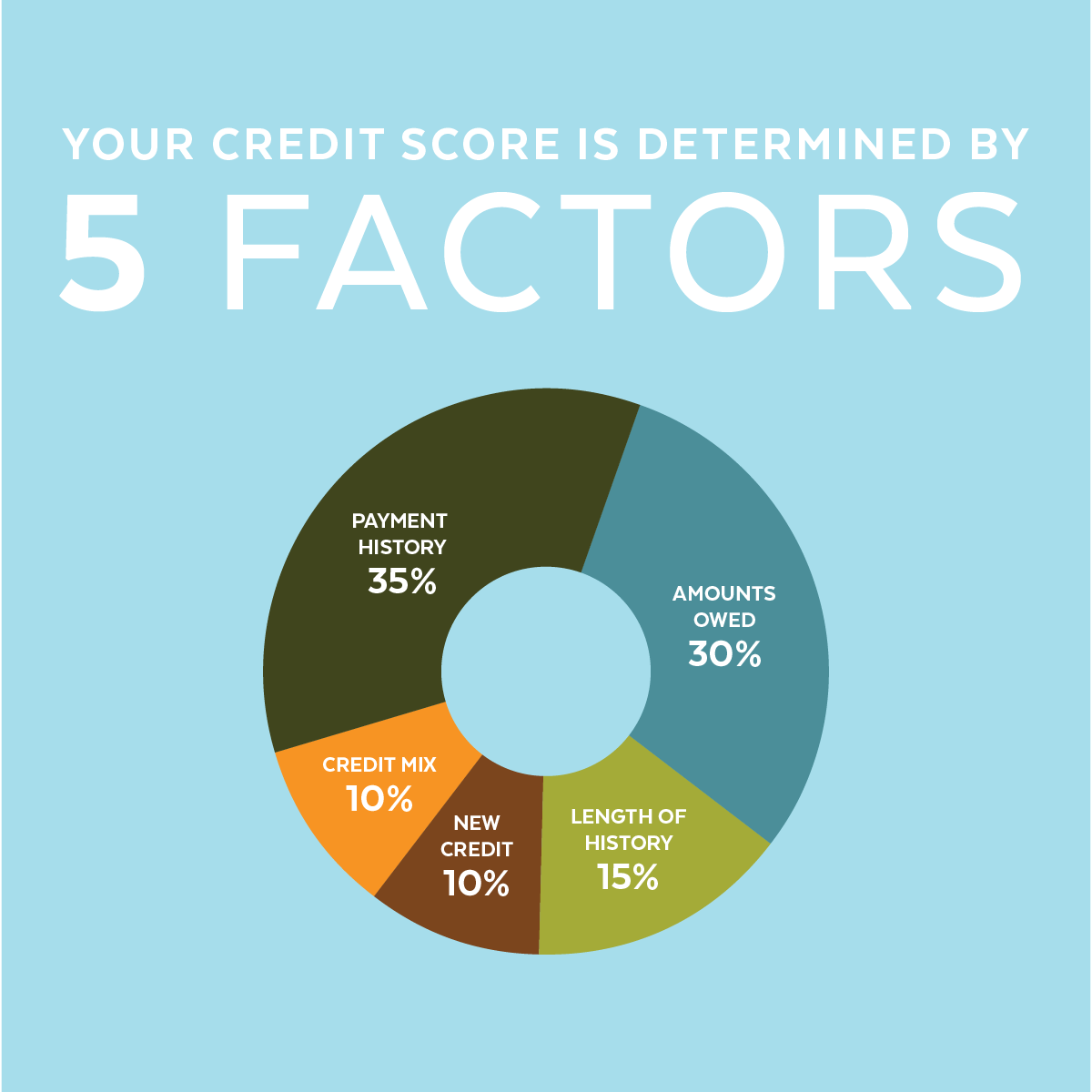

FICO scores are based on five categories. The chart below shows the relative importance of each category.

Payment history – 35%

Your payment history is the most important factor when it comes to the FICO scoring system; checking whether you paid your bills on time. This payment history is reviewed across the different types of accounts a person might have utilized at one point, such as credit cards, retail accounts, installment loans, and finance company accounts. This category also includes bankruptcy and collection items history.

Amounts owed – 30%

The second most important factor in a FICO score is the amount of credit and loans you are using. They’re looking at your credit utilization and any outstanding balances that you have on installment loans compared to the original amount.

Credit utilization is one of the most important factors evaluated in this category. Credit utilization is the ratio of the balance owed compared to the credit line’s limit. While lenders determine how much credit they are willing to provide, you control how much you use. A higher credit utilization ratio may point toward difficulties in money management.

FICO research shows that people using a high percentage of their available credit limits are more likely to have trouble making some payments now or in the near future, compared to people using a lower level of available credit.

Having credit accounts with an outstanding balance does not necessarily mean you are a high-risk borrower with a low FICO score. A long history of demonstrating consistent payments on credit accounts is a good way to show lenders you manage your finances responsibly.

Length of credit history – 15%

How long you’ve had credit is the third most relevant factor. A general rule of thumb is, a longer credit history will increase your FICO score. However, even people who have not been using credit long can have a good FICO score, depending on the other factors mentioned above. To determine the length of credit history, they will consider the age of the oldest account, the age of the newest account, and an average age of all credit accounts. The last time you used the account is also taken into consideration.

New credit – 10%

About 10 percent of FICO is based on the frequency of credit inquiries and new account openings. According to FICO research, someone who opens several credit accounts in a short period of time could be a greater risk investment compared to others. This category also includes any recent requests of credit that have been made, and whether you have a good recent credit history following any past payment problems.

If you’re currently looking for an auto, mortgage or student loan that may prompt multiple lenders to request your credit report, don’t sweat it! FICO scores will disregard auto, mortgage, and student loan inquiries made within 30 days. Therefore, multiple inquiries won’t affect the scores of consumers who apply for a loan within the month.

If your search is extended for more than 30 days, you may want to consider waiting to apply all at once. FICO scores typically count inquiries of the same loan type that fall within a typical shopping period as just one inquiry when deciding your score.

Credit mix – 10%

And finally, 10 percent of one’s FICO score is based on the type of credit in use, such as installment loans, finance company accounts, mortgage loans, and retail store accounts. It is not necessary to have one of each, and it is not a good idea to open a credit account you don’t intend to use. In this category, FICO takes into account the type of credit accounts on the report and how many establishments you have in total. For different credit profiles, what’s considered a healthy mix will vary depending on your overall credit picture.

What is a good FICO score?

The general rule of thumb is the higher score, the better. FICO scores range from 300 to 850, where higher scores display lower credit risk and vice versa (note: some types of FICO scores have a slightly broader range). What’s considered a “good” FICO score varies since each lender has its own standards for approving credit applications. These standards are based on the level of risk they find acceptable. Therefore, one lender may offer its lowest interest rates for a higher score.

Here is a quick chart to provide a breakdown of ranges for the FICO score:

It may be a good idea to check with your lender what they consider a good FICO score for a specific application before applying.

Can I get my credit report for free?

Yes. You may get a free copy of your credit report once every 12 months from each of the three major consumer reporting agencies annually: Experian, TransUnion, and Equifax.

You can visit www.annualcreditreport.com to request a copy of your credit report. Please note that your free credit report will not include your FICO score. Because your FICO score is based on the information in your credit report, it is important to make sure that the credit report information is accurate.

I’m new to credit, what is my FICO score?

FICO Scores are generated by complex calculations based on unique credit report data, so there is no “typical” or “entry-level” score. While someone new to credit may have difficulty scoring in the highest score ranges due to a limited number of active accounts and length of history, it is possible to have a FICO score that meets lenders’ criteria for granting credit. FICO scores consider the extent to which people can demonstrate a good track record of making payments on time. In fact, payment history is more important for FICO scores (about 35 percent) than the length of credit history (about 15 percent).

Will it hurt FICO scores if I apply for new credit?

It may affect your FICO score, but it probably won’t drop much. If you apply for a credit account, a request for your credit report information (called a “hard inquiry”) will appear on your report.

How does a FICO score help you?

Keep in mind that FICO scores are only one of many factors lenders consider when making a credit decision. FICO scores may benefit you in just some of these ways:

Get credit faster: FICO scores can be delivered almost instantaneously, helping lenders speed up credit card and loan approvals.

Unbiased credit decisions: Factors such as your gender, race, religion, nationality and marital status are not considered by FICO scores. When a lender uses your FICO score, they’re getting an evaluation of your credit history that is fair and objective.

May save you money: A higher FICO score can help you qualify for better rates from lenders. Generally, the higher your score, the lower your interest rate and payments.

More opportunities: Lenders can evaluate the associated risk levels more accurately with a FICO score, therefore they may be able to offer different prices and rates to different borrowers. Rather than offering “one-size-fits-all” credit products, lenders use FICO scores to consider consumers who might have been declined credit in the past.

If you’re starting out or want to improve your score, consider meeting with an Empeople Financial Wellness Manger today. Our free ongoing financial guidance program help you to get the credit score you need to meet your financial goals faster.