How Does Refinancing Work and When To Refinance My Mortgage

There are many reasons as to why you should consider refinancing. As with any financial decision, arming yourself with knowledge of how refinancing works, its benefits and risks is always a good practice. You could potentially save yourself a hundred or two every month. Now that’s some significant savings that could be invested elsewhere.

What is mortgage refinancing?

Mortgage refinancing in a nutshell means paying off your current mortgage so as to get a new mortgage with lower interest rates, a shorter repayment term or changing from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage. Mortgage refinancing also allows the opportunity to cash-in to your home’s equity or even to consolidate your debts.

However, there are some costs that you must be aware of before looking to refinance. You’d be responsible for appraisal, application fees and closing costs which translates to roughly 3-6% of the mortgage principal[1]. Now you may ask: Is that worth it? That is the question that we will strive to help you answer today.

As always, it’s recommended to speak to a mortgage advisor for specialized advice to your unique financial situation. At Empeople, we are proud to have our own dedicated mortgage team who are qualified and prepared to help make this complex decision a breeze!

Who qualifies for a mortgage refinancing?

Lender and credit unions typically require a loan-to-value (LTV) ratio of 80% or less to qualify for refinancing[2]. LTV ratios are calculated by taking your remaining mortgage balance divided by your home value. For example, if your remaining mortgage balance is $100,000 and the value of your house is $150,000, your LTV ratio is 66.67%.

3 types of mortgage refinancing and which one is the right one for you

3 types of mortgage refinancing and which one is the right one for you

1. Rate & Term Refinancing

Rate & term refinancing is the most basic and common form of mortgage refinancing. How it works is by taking your current mortgage and replacing it with a new one to obtain a better mortgage rate and repayment term.

Who this is good for: Anyone who is looking to lower their interest rates and to lower their monthly payments. Typically, after at least 6-months of homeownership[3].

To better illustrate how much you could save, try giving our refinance calculator a go if you’re wondering whether it’s the right time to refinance.

2. Cash-Out Refinancing

This type of refinancing occurs whenever your home equity rises by an amount that you would like to “cash-out” a portion of. For example, let’s say you bought your first family home and took a mortgage out on it for $300,000. You’ve been diligently paying off your mortgage monthly and now you’re just left with $200,000 to pay for. That equates to $100,000 in home equity that you’ve built up.

That’s $100,000 in home equity that you could potentially convert a portion of it into cash. Most lenders allow borrowing up to 95% of the home equity that you’ve built up[4]. In this case, that’s $100,000 x 95% = $95,000.

If you’re looking to convert $50,000 into cash, that would mean refinancing to take out a new loan for $250,000 ($200,000 – remaining mortgage balance + $50,000 – desired cash). Thus, the new mortgage principal after the cash-out refinance would be $250,000.

Who this is good for: People who have built up home equity and would like to access a large amount of cash to put into larger expenses such as home improvements or college tuitions.

3. Cash-In Refinancing

A cash-in refinance works when you pay down your existing mortgage to under a certain loan-to-value (LTV) ratio in order to qualify for a mortgage refinance.

Let’s use an example to illustrate this better.

Current mortgage balance: $320,000

Current home value: $300,000.

LTV ratio: 107%.

In order to qualify for a traditional rate and term refinance, lenders ideally like to see your LTV ratio fall to about 80% or below[1]. You have a LTV ratio of 107%, so you don’t quite qualify for a refinance. So, what can you do about it?

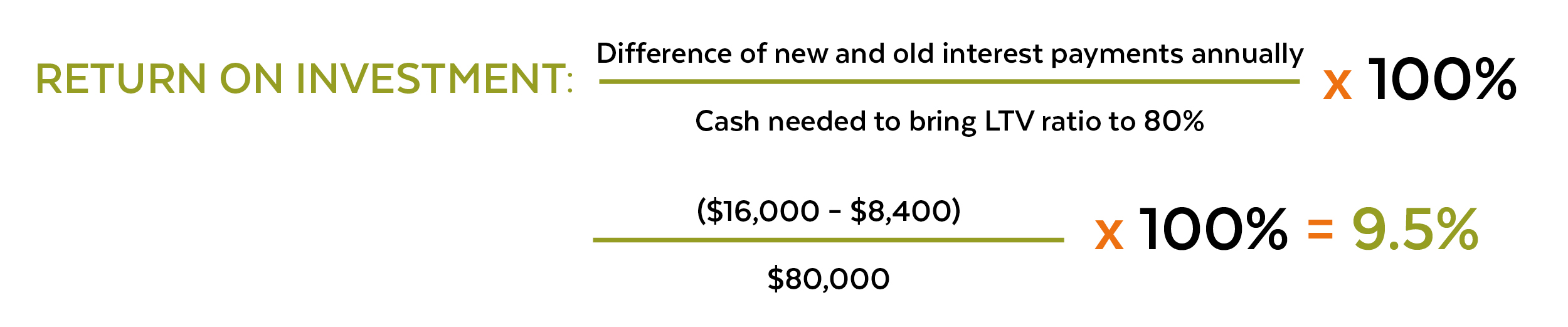

This is where cash-in refinancing could help you. You could inject in some cash into your mortgage loan to bring it down to the 80% threshold. By our calculations, you’d need you to bring your mortgage balance down to $240,000 from $320,000. Meaning that you’d need to inject in $80,000 in cash to meet the minimum requirements.

Let’s say your lender works a deal with you to bring your mortgage rates down from 5% to 3.5%, only if you meet the 80% LTV ratio threshold. Is that worth the cash-in investment? Let’s find out.

The only figures you need are your old vs. new annual interest payments. After using a mortgage calculator, we found that:

Old annual interest payments for $320,000 @ 5%: $16,000

New annual interest payments for $240,000 @ 3.5%: $8,400

A 9.5% rate of return is considered a pretty good investment in today’s market, given that you’re guaranteed that specific rate of return no matter what happens.

A 9.5% rate of return is considered a pretty good investment in today’s market, given that you’re guaranteed that specific rate of return no matter what happens.

Who this is good for: Borrowers whose home equity has dropped whereby their LTV ratio is above 80% threshold. Borrowers who also sit on a fairly large amount of cash savings and are looking to see if a cash-in refinance deal is a good option for a solid return on investment.

When to refinance?

When to refinance?

A rule of thumb to abide by is that if you’re able to reduce your interest rates by roughly 1% to 2%, then it may be worthwhile to consider refinancing[1]. Remember, your total savings with the new rates must cover the many fees (appraisal, applications, closing costs, etc.) during refinancing to make it a worthwhile endeavor.

When looking at a cash-out refinance however, there are no hard rules for when it’s a good time. Taking out the cash from your home’s equity and investing it elsewhere could be risky but could also be very lucrative. The same applies for a cash-in refinance, where you’d have to crunch the numbers to see whether the returns are worth it.

If you’re still unsure that a mortgage refinance is a good choice for you, you can contact our mortgage team for an expert’s second opinion. Remember that all loans are subject to approval, so give our team a call or get pre-approved using our online application.

In conclusion, when making the decision to refinance your mortgage, be aware of the options, the fees and the risks involved. Spend some time crunching the numbers, because it could potentially save you thousands and open up other lucrative opportunities for you and your family.

This article has been provided for educational purposes only and is not intended to replace the advice of a loan representative or financial advisor. Empeople does not provide tax advice. The examples provided within the article are for example only and may not apply to your situation. Since every situation is different, we recommend speaking to a loan representative or financial advisor regarding your specific needs. You may also want to contact your tax advisor for additional tax information.

References

[1] – Investopedia – When and When Not to Refinance Mortgage

[2] – Investopedia – Loan to Value

[3] – Total Mortgage – Refinance Mortgage Soon After Purchase