Millennial Budget Tips To Pay Down Debt

One question we hear most often from Credit Union members is “How do I get out of debt?” It comes up constantly in conversations and now seems more present than ever.

So, I had to ask myself . . . “why this question?” and after some serious research into it, I found a one-word answer that astonished me:

Millennials!

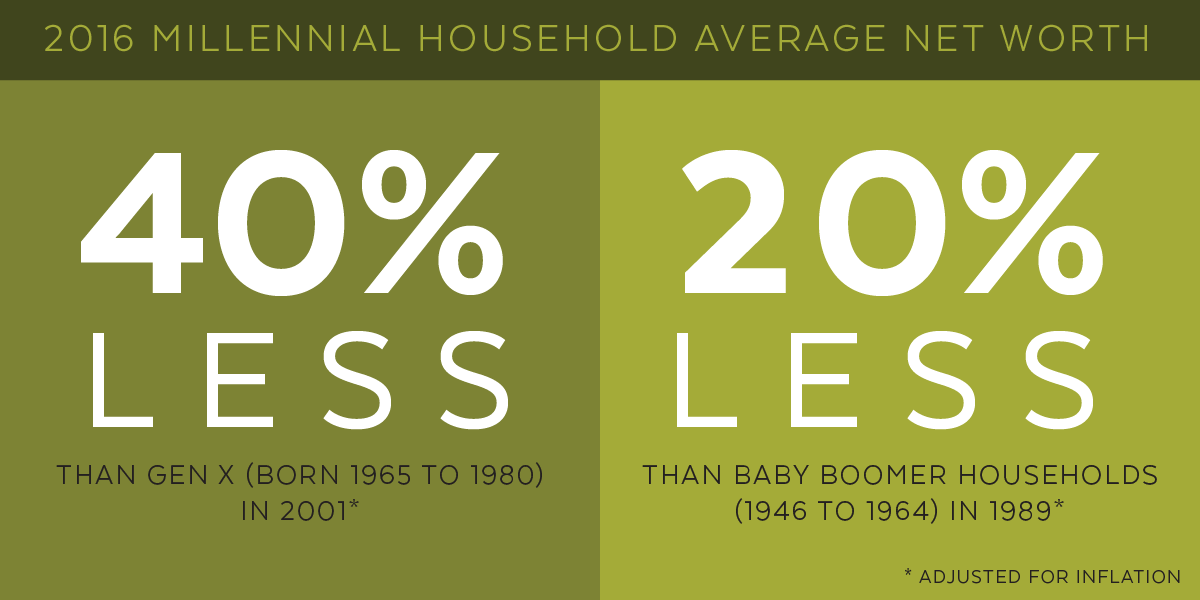

Born between 1981 and 1996, Millennials are the chief drivers of America’s debt revolution. The Federal Reserve gathered data and released statistics that showed 2016 Millennial households to have an average net worth around $92,000, about 40% less than Gen X (born 1965 to 1980) had in 2001, adjusted for inflation, and about 20% less than similarly-adjusted baby boomer households (1946 to 1964) had in 1989.

But why are Millennials in debt? Well, let me hit you with what I consider the top 3 reasons:

1. Rising student debt.

Since 1978, Labor Department shows college tuition growing at more than four times the rate of overall inflation. The average cost of a Bachelor of Science or Arts diploma from a private college in 2019 is $96,460 more than it was in 1979, according to the College Board. That’s an inflation rate of 1,375%. Speaking as a millennial, the topic of student loan debt is something that comes up constantly in our household. My wife and I both went to college right out of high school, but neither of us knew what we wanted to do in life. Each of us jumped majors multiple times which essentially hit the “restart” button on our education each time. Once we got to 4 years in college, we realized we were so far behind that the idea of graduation was years away. Ultimately, at that time in our lives we decided school wasn’t for us and left without finishing our education. Forbes recently published that Millennials carry an average $33,000 in student debt. And the New York Federal Reserve did research that showed four in 10 recent college graduates are in jobs that don’t even require degrees.

Years later, we’ve both been working and accumulated the debt that comes with life (homes, cars, etc). It was at this point that we decided to go back to school to finish up our degrees; we both worked full time while going to school, but because of “life” our income went to living expenses and not to pay for school…so we added more student loans to our bottom line. While this was a great move for our careers, financially…not so much.

The New York Reserve also said student loan debt has quadrupled since the start of 2005 to $1.48 trillion, rising faster in those 14 years than all other categories of household credit. And since 2013 at least 2 million borrowers have defaulted their loan obligations. This is why this is #1 on my list!

2. The cost of living is going through the roof.

Harvard University ran the numbers and came back to interpret data that shows a statistically average U.S. house now costs four times as much as the statistically average American worker earns annually. From 1980 to 1999, home prices were closer to three times household income.

When I first moved to the area I live now, I wasn’t sure where I wanted to ultimately land so I rented. I wasn’t a fan of locking myself into long term leases, so I would sign 6 to 12 month max leases and move. The part that amazed is that each time I moved my rent seemed to increase by $150 to $200! After a few years of this, the idea of buying a house went from a pipe dream to a must if I was going to stay living in the area.

3. Why does it take so long to save?

Since 1978, inflation in America has averaged around 3.40% and the equivalent purchasing power of a hundred dollar bill 40 years ago is now about $393.80 in today’s money. Millennials, with a lower average annual income of around $35,000, will need more than 20 years to save enough for a 20% down payment on a statistically average-priced condo in their equally statistically averaged real estate market.

These three factors equate to a serious cash-flow problem for the younger generation, so much so that 1 in 5 millennials expect to still be in debt when they die.

Now, do you understand why so many of us deal with anxiety?

That’s right, I said “us” because I am part of the Millennial Generation. I have watched debt and income issues like this play havoc on friends and family for years. And the only upside from my vantage point as a financial professional is that I have a unique ability to help guide individuals like ‘us’ to financial freedom.

So, let’s get started!

The first thing you need to do when learning to beat debt is to learn how to budget!

What is a budget you say? Essentially, a budget is your guide to what kind of income you have coming in and what kind of expenses have gone out. Once you have a handle on your expenses, you’ll be able to dedicate more money to pay off debt, like student loans. Here is my sure-fire way to build a budget:

1. Grab your last 30 days’ worth of pay stubs.

Get this from your employer’s self-service portal, or your HR department.

This will tell you what your average monthly income is. Do not count overtime at your job into your budget; OT-pay is bonus income!

2. Log into Empeople Digital Banking and download the last 90 days of charges. Depending on what kind of spender you are, you may need to look at both your debit card and credit card for this information.

Now, break these charges into 5 or 6 basic categories like home, auto, groceries, child-care, fun and dining out, etc.

Total each category and divide by 3 to get your itemized average monthly expenses.

Now you have a base to start from; you know how much you make and spend during an average month.

3. Next, look for outliers. Look at your expenses and ask yourself, “does that seem like a lot of money to spend on…dining out?” If the answer is yes, set a dollar amount you would like to spend per month and try it out.

Word to the wise, do not get overly aggressive here, it’s better to project high and come in low than to project low and overspend.

But how does this newly-built budget help you pay down debt more quickly? Once you know how much you should be spending a month, you will know how much of your income you should have leftover. For example, your budget says you make $2,200 a month, but you only spend $1,800; that would mean you have $400 a month left over to pay down debt!

This brings me to the most important part of budgeting: PAY YOURSELF FIRST!

The moment you get paid, take that $400 and pay it towards debt immediately! Do not wait until the end of the month to see what you have leftover and put that towards debt or savings. It’s too easy to overspend if you know you will have a cushion at the end of the month. By paying down on debt right away you remove that cushion and force yourself to stick to your budget.

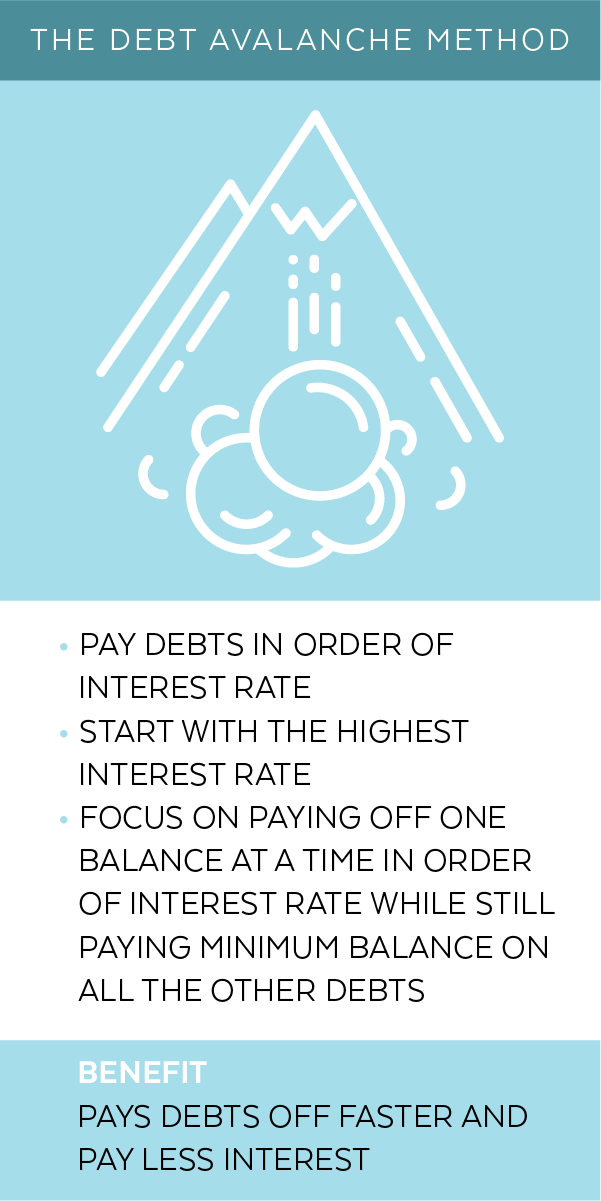

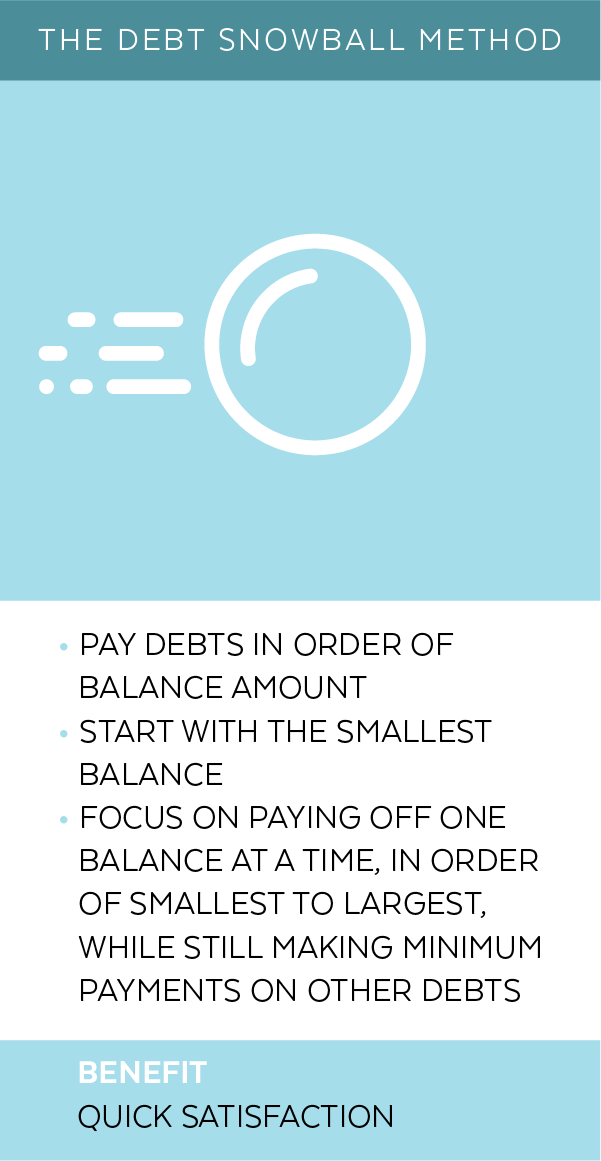

You can pay down debt by using the snowball or avalanche method. Check out the image below to see the difference between the two and decide which method will work best for you.

After a few months, re-evaluate your budget and see how you’re doing. Are you overspending? Are you not spending as much as you thought? Adjust your habits accordingly and again, pay your debts first and re-evaluate after a few more months.

Once you have done this for about 6 months you should have an ironclad budget. Now the only thing you have left to do is watch your debts wither away!

It took about 6 months for me to get a handle on the size of my family expenses. And in the middle of it, my wife and I realized we were eating out too often and watching groceries rot in our fridge. We learned to buy food in smaller amounts, plan out meals, avoid wasting food and stop overspending on restaurants and delivery.

Budgeting is important and something every individual and family should have. Some find it easy, while others find it difficult, but know that you’re not alone in the struggle. There are tons of free online budgeting tools and apps that you can take advantage of. Here at Empeople, we offer a free budgeting tool through Digital Banking called Money Manager. It not only offers budgeting but account aggregation, alerts, categorization, a bill and income calendar, goal management, tracking, and more! Give it a try by logging into Digital Banking, select the Services Tab and then Money Manager.

Want some more help with budgeting? At Empeople we are always here for you. Empeople’s number one concern is our members’ finances, reach out with any questions you have or try out our self-serve online financial education program.

Sources:

- Wesley Whistle, “A Look At Millennial Student Debt” Forbes , October 3 , 2019.

- Hillary Hoffower, “7 ways life is more expensive today for American millennials than previous generations” Business Inside, May 28, 2018.

- Up to Us, “Do Millennials Earn Less Than Previous Generations” Medium, July 22.

- Megan Leonhardt, “1 in 5 millennials with debt expect to die without ever paying it off” Become Debt Free, January 9 , 2019.